This guide covers the meaning and mechanics behind code 05 declines, the risk factors that elevate decline rates for high-risk industries, systematic diagnostic methods for identifying root causes, proven recovery and routing solutions, conversion-protection strategies, and how specialized payment support can resolve persistent decline patterns.

Code 05 acts as a catch-all response that can mask dozens of underlying issues, from insufficient funds and expired cards to fraud flags and issuer-level velocity limits. Understanding what triggers this generic refusal is the first step toward fixing it.

High-risk merchants face compounded challenges because their industry classification alone raises issuer scrutiny. Chargeback histories, card-not-present transaction volumes, and payment method mismatches all feed into elevated decline rates that generic processors rarely address.

Diagnosing these declines requires structured analysis of transaction logs, processor response data, and merchant account configurations. Patterns in timing, card type, geography, and BIN ranges often reveal the true cause behind a vague “Do Not Honor” response. Once root causes surface, targeted fixes like smart retry logic, dynamic payment routing, enhanced verification protocols, and proactive customer communication can recover failed transactions and protect approval rates long term.

What Does a “Do Not Honor” Decline Mean in Payment Processing?

A “Do Not Honor” decline is a generic refusal from the issuing bank that blocks a transaction without providing a specific reason. This section covers why card issuers use this error code and which transaction scenarios trigger it most often.Why Do Card Issuers Use the “Do Not Honor” Error Code?

Card issuers use the “Do Not Honor” error code as a catch-all response when they decide to block a transaction but choose not to disclose the exact reason. The decline can stem from insufficient funds, expired card details, suspected fraud, or internal risk thresholds that the issuer does not share with the merchant.This lack of specificity creates a significant diagnostic challenge. According to a 2024 Baremetrics analysis, payment failures caused by expired cards, insufficient funds, or processing errors can impact Annual Recurring Revenue by as much as 10%. Because issuers bundle multiple rejection reasons under one vague code, merchants are left to investigate each decline individually rather than applying a single fix. For high-risk merchants especially, this opacity compounds the difficulty of maintaining healthy approval rates.

What Are the Most Common Transaction Scenarios Triggering This Decline?

The most common transaction scenarios triggering this decline include recurring billing charges, high-ticket purchases, cross-border transactions, and first-time orders from new customers. Each scenario presents a distinct risk signal that issuing banks evaluate against their internal fraud and credit models.Recurring billing is particularly vulnerable. According to WallID, approximately 15% of credit card payments tied to recurring billing are declined, and in some sectors, this number exceeds 30%. Meanwhile, a 2025 PYMNTS report found that 47% of retailers say false declines impact consumer satisfaction, since consumers expect seamless transactions and payment friction leads to abandoned purchases. For merchants processing subscription-based or repeat transactions, these “Do Not Honor” responses often represent legitimate customers whose payments are blocked unnecessarily, making decline debugging essential for protecting both revenue and customer relationships.

What Are the Leading Causes of “Do Not Honor” Declines for High-Risk Businesses?

The leading causes of “Do Not Honor” declines for high-risk businesses include elevated industry risk profiles, mismatched payment methods, and issuer-level preferences that flag certain merchant categories. The sections below examine how industry classification and payment method selection each drive decline rates.How Do Industry-Specific Risk Factors Contribute to Decline Rates?

Industry-specific risk factors contribute to decline rates by triggering stricter issuer screening for merchant categories associated with chargebacks, regulatory complexity, and fraud exposure. Adult entertainment, for example, is considered a high-risk merchant category because of age restrictions, legal implications, and high chargeback rates. According to PayAtlas, the adult content industry faces chargeback rates often twice that of other sectors, which directly impacts payment service provider profitability and risk exposure.When issuers detect transactions from these flagged categories, their fraud models apply tighter thresholds, increasing the likelihood of a generic “Do Not Honor” response. AI-powered tools are beginning to address this imbalance; Mastercard’s Decision Intelligence platform reduced false declines by 85 percent while maintaining high fraud detection rates. For high-risk merchants, pairing industry-aware fraud tools with processors experienced in their vertical is one of the most effective ways to lower unjustified declines.

Specialized payment processors like 2Accept pair dedicated payment experts with fraud management tools designed specifically for high-risk verticals, helping merchants in sectors like telemedicine, firearms, and Hemp and CBD optimize their authorization rates while maintaining security.

In What Ways Do Payment Method Types and Issuer Preferences Affect Declines?

Payment method types and issuer preferences affect declines by creating mismatches between how a customer pays and what the issuing bank is willing to authorize. Issuers evaluate each transaction against card type, network rules, and regional preferences. When a merchant only supports a narrow set of payment methods, transactions routed through less-preferred channels face higher rejection rates.According to a 2025 Baymard Institute analysis, up to 17 percent of shoppers abandon carts if their preferred payment method is not available. Offering local and alternative payment options reduces this friction significantly. Over 80 percent of businesses adopting payment orchestration report an improved customer experience through support for local methods and more reliable checkout processes.

For high-risk merchants, especially those like offshore businesses, diversifying accepted payment types, including digital wallets and regional options, gives issuers fewer reasons to flag transactions as suspicious. Understanding how issuer preferences and payment orchestration intersect helps merchants diagnose whether their decline problem is rooted in risk profiling or checkout configuration.

How Can Merchants Systematically Diagnose “Do Not Honor” Errors?

Merchants can systematically diagnose “Do Not Honor” errors by analyzing transaction logs for patterns and gathering targeted insights from their merchant account configuration. The following subsections cover the most useful data points and the essential steps for extracting actionable intelligence.Which Data Points and Logs Are Most Useful for Root Cause Analysis?

The data points and logs most useful for root cause analysis include gateway response codes, timestamps, card BIN ranges, transaction amounts, and customer geographic data. Correlating these fields reveals whether declines cluster around specific issuers, time windows, or ticket sizes. Key data points to extract from transaction logs:- Response code and sub-code: Distinguish code 05 from other soft or hard declines to isolate true “Do Not Honor” patterns.

- Card BIN (first 6-8 digits): Identifies the issuing bank, exposing issuer-specific decline tendencies.

- Transaction amount and currency: Flags threshold-triggered blocks where issuers cap single-transaction values.

- Timestamp and frequency: Reveals velocity-based rejections, common in card testing, when multiple charges hit the same card in a short window.

- AVS and CVV match results: Mismatches often precede a generic code 05, masking an addressable data-quality issue.

What Are the Essential Steps for Gathering Merchant-Account Insights?

The essential steps for gathering merchant-account insights are reviewing processor configuration settings, requesting detailed decline-reason reports from your acquirer, and benchmarking your authorization rate against industry standards.- Request granular decline reports from your payment processor, broken down by decline codes, card network, and issuer.

- Audit MCC assignment to confirm your merchant category code accurately reflects your business type; a misclassified MCC triggers disproportionate issuer scrutiny.

- Review fraud-filter thresholds in your gateway dashboard, since overly aggressive velocity or geolocation rules generate false positives that surface as code 05.

- Compare authorization rates to benchmarks; according to Worldpay, the average global card authorization rate is 85-90%, with optimized merchants achieving 91-96%.

- Engage your acquirer’s risk team directly to identify account-level flags or processing restrictions that silently elevate decline rates.

What Real-World Solutions Successfully Resolve “Do Not Honor” Declines?

Real-world solutions that successfully resolve “Do Not Honor” declines include strategic retry logic, payment routing optimization, and enhanced verification methods. The following subsections break down when to retry versus escalate, how processor changes lift approval rates, and where alternative payment methods recover lost revenue.When Should You Retry a Transaction Versus Escalate for Review?

You should retry a transaction when the decline appears to be a soft decline, meaning the issue is temporary and may resolve on a subsequent attempt. Hard declines, where the issuer firmly rejects the payment, require escalation rather than repeated attempts.The distinction matters because retrying a hard decline wastes processing resources and can trigger fraud flags. According to Spreedly’s research published through the Merchant Risk Council, 7.9% of failed transactions succeed when retried immediately through a secondary gateway. That modest recovery rate adds up quickly at scale, but only when retries target the right failures.

A practical approach involves categorizing each decline response before acting:

- Soft declines (temporary holds, timeouts, issuer unavailability) warrant an automatic retry after a brief delay.

- Hard declines (stolen card, closed account, permanent blocks) should route to manual review or customer outreach.

- Ambiguous “Do Not Honor” responses benefit from one retry with adjusted parameters, such as a different gateway or time window, before escalating.

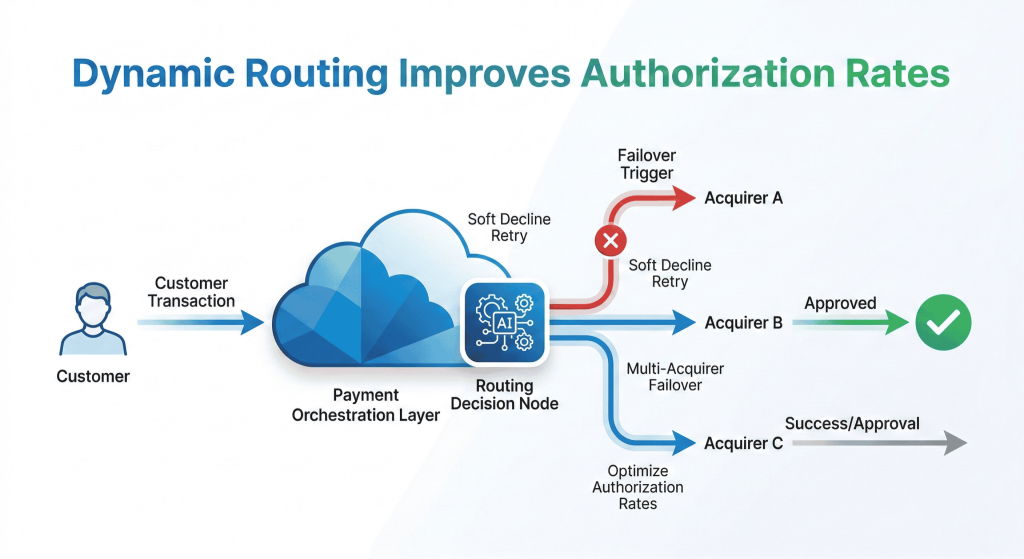

How Do Payment Routing or Processor Changes Impact Approval Rates?

Payment routing and processor changes impact approval rates by directing transactions to the acquirer or gateway most likely to receive issuer approval. Dynamic routing evaluates factors such as card type, issuer region, and transaction amount in real time, then selects the optimal processing path.According to the Capgemini Research Institute, payment orchestration improves merchant authorization rates by 2 to 3 percent on average through dynamic routing to best-performing providers. For businesses processing millions in monthly volume, that incremental lift translates directly into recovered revenue.

Key routing strategies that reduce “Do Not Honor” declines include:

- Multi-acquirer failover, which automatically reroutes a declined transaction to a secondary processor.

- Region-matched routing, which sends transactions to acquirers with stronger relationships to the cardholder’s issuing bank.

- Intelligent retry scheduling, which staggers reattempts based on issuer behavior patterns.

What Role Do Enhanced Verification or Alternative Methods Play in Recovery?

Enhanced verification and alternative payment methods play a critical role in recovery by addressing the root causes behind issuer-level blocks. When a card transaction triggers “Do Not Honor,” the issue often stems from insufficient authentication data or issuer-side risk scoring that flags the merchant or transaction type.Enhanced verification tools reduce these friction points:

- 3D Secure authentication provides issuers with additional cardholder verification, shifting liability and increasing issuer confidence in approving the transaction.

- Address Verification Service (AVS) and CVV matching supply data points that help issuers distinguish legitimate purchases from potential fraud.

- Tokenized credentials replace raw card data with secure tokens, reducing the likelihood of security-triggered declines on recurring charges.

For high-risk merchants, layering strong verification with diverse payment options creates a safety net that traditional single-processor setups cannot match. With these recovery strategies in place, proactive prevention becomes the next priority for protecting conversion rates.

How Can Merchants Prevent “Do Not Honor” Declines from Impacting Conversion?

Merchants can prevent “Do Not Honor” declines from impacting conversion through proactive customer communication and strategic account configuration. The following subsections cover messaging tactics that reduce friction and setup choices that lower decline risk.What Communication Strategies with Customers Help Reduce Decline Friction?

Communication strategies with customers that help reduce decline friction include pre-payment reminders, real-time error messaging, and structured dunning sequences. According to Baymard Institute research, nearly 70 percent of online shopping carts are abandoned on average globally, with payment friction cited as a leading cause. Much of that friction stems from unclear decline messaging that leaves customers confused and unwilling to retry.Effective approaches include:

- Sending reminder notifications before recurring charges so customers can update expired cards or confirm sufficient funds.

- Displaying clear, specific error messages at checkout that guide the customer toward a resolution, such as “Please try a different card” rather than a generic failure notice.

- Using automated dunning sequences with scheduled retries for subscription billing, spacing attempts over several days to catch temporary issues like insufficient funds.

- Providing alternative payment options directly on the decline screen so customers can complete the purchase immediately.

Which Preventative Account Setup Choices Minimize Risk of This Decline?

The preventative account setup choices that minimize risk of this decline center on merchant account classification, fraud tool calibration, and processor diversification. Card-not-present fraud accounts for over 80 percent of all card fraud globally, according to Europol’s 2023 Internet Organised Crime Threat Assessment, which means issuers scrutinize CNP merchants more heavily and trigger “Do Not Honor” responses more frequently.Key setup decisions that reduce decline exposure include:

- Selecting a merchant category code (MCC) that accurately reflects your business to avoid issuer risk flags from misclassified accounts.

- Calibrating fraud filters to avoid overly aggressive thresholds that block legitimate transactions alongside fraudulent ones.

- Implementing 3D Secure selectively for high-value or high-risk transactions, shifting liability while preserving approval rates on routine purchases.

- Maintaining relationships with multiple payment service providers so transactions can route through alternative acquirers when one path declines.

With these preventative measures in place, partnering with a specialist processor adds another layer of protection.

How Does 2Accept Support High-Risk Merchants Facing “Do Not Honor” Declines?

2Accept supports high-risk merchants facing “Do Not Honor” declines through dedicated payment experts, tailored fraud and chargeback management, and hands-on decline resolution. The following sections cover how personalized support reduces these issues and the key takeaways from this guide.Can Dedicated Payment Experts at 2Accept Help Reduce and Fix “Do Not Honor” Issues?

Yes, dedicated payment experts at 2Accept can help reduce and fix “Do Not Honor” issues. Every client receives a personal payment specialist who analyzes decline patterns, identifies root causes, and builds a tailored recovery strategy. Rather than routing merchants through chatbots or generic support queues, 2Accept assigns real people who understand high-risk verticals like telemedicine, firearms, Hemp and CBD, auto dealerships, and vape businesses.According to a 2023 report by the Merchant Risk Council, the average ecommerce chargeback rate ranged between 0.6 and 0.9 percent of transactions, with certain high-risk categories exceeding 1.5 percent. These elevated rates make proactive decline management essential. 2Accept addresses this through specialized fraud and chargeback management tools combined with compliance services designed for high-risk industries. This white-glove approach treats each merchant’s payment stack as a unique system rather than a one-size-fits-all configuration.

What Are the Key Takeaways About Decline Debugging: Mapping “Do Not Honor” to Real Fixes We Covered?

The key takeaways about decline debugging are that “Do Not Honor” declines require systematic diagnosis, targeted fixes, and ongoing prevention. Throughout this guide, we covered several actionable principles:- “Do Not Honor” (code 05) is a generic issuer refusal that masks multiple underlying causes, from insufficient funds to fraud flags.

- High-risk industries face disproportionately higher decline and chargeback rates, making specialized processing partnerships critical.

- Smart retry logic, payment routing adjustments, and enhanced verification methods each recover revenue that would otherwise be lost.

- Proactive customer communication, including pre-charge reminders and dunning sequences, reduces involuntary churn before it starts.

- Preventative account setup choices, such as proper MCC classification and robust fraud screening, minimize future decline exposure.